Why is it so difficult (and crazy expensive) to fly within Africa?

Thinking through the economics and politics of connectivity in a vast Continent

Thank you for being a regular reader of An Africanist Perspective. If you haven’t done so yet, please hit subscribe to receive timely updates on new posts along with over 35,000 other subscribers. New regular content is free. Book reviews and the archives are gated.

I: Intra-African air travel is insanely expensive (and yet African airlines barely make any profits)

Over the last year I’ve visited several cities in East, West, Southern, and North Africa; and let’s just say that it’s insanely expensive to travel by air within Africa. In addition, the connections often don’t make much sense (only 19% of intra-African connections have direct flights). For example, to fly to Rabat from Nairobi my best connection was through Paris. While there has been tremendous improvement with regard to intra-Africa visa waivers, a lot more needs to be done to ease costs and increase efficiencies in the regional aviation market. Consider this story from Bloomberg:

A 45-minute flight from Ghana to neighboring Lagos can cost $600. Flights to Dakar,Senegal, require a full day of travel with a four-hour layover in Abidjan, in Côte d’Ivoire. A roundtrip fare to Casablanca is about $1,800, while discount carriers reach the city from Spain for as little as €50($57). That’s without factoring in the frequent delays and breakdowns of small aircraft of varying quality.

What explains this? Lots of reasons. Bad infrastructure (especially on air navigation); high taxation per ticket (including airport facility fees and navigation charges); mismanagement of airlines (especially those SOEs operated as prestige flag carriers); blocked funds (when countries prevent airlines from repatriating earnings); high cost of capital (no doubt impacted by sovereign credit worthiness); maintenance and supply chain pressures (African airlines’ planes tend to be 5 years older than the global average — which means less fuel efficiency, higher frequency of maintenance, and costly aircraft downtime and delays); and low volumes (a function of economic under-development and little intra-African economic integration).

That’s before we even get into the fact that it’s mighty hard to run a successful airline anywhere in the world. Yet even with that it mind, the comparative data suggests that African economies are leaving a whole of cash on table.

This is plainly on account of bad policies borne of a lack of strategic awareness and related anti-development interest group politics. The inability to effectively coordinate on aviation policy across the Continent is yet another example of Pan-Africanism as summitry and protocols, and little more (and why we need to reconceptualize the operationalization of Pan-Africanism).

A combination of policy failures and industry economics forces African airlines to have very tight margins and to pass the high cost of doing business to customers. The IATA provides a useful summary:

Fuel prices: +17% higher, Taxes and charges: +12–15% higher, Air navigation charges: +10%, Maintenance, insurance, and capital costs: +6–10%.

…. Of the $41 billion in global net profit forecast for 2026 (3.9% margin), African carriers are expected to generate just $200 million profit, representing a 1.0% margin—the lowest of all regions. This equates to $1.3 in profit per passenger, compared to a global average of $7.9. [The average for the Middle East’s airlines is $28.60].

Despite all this, Africa (as a region) is projected to see 4.1% average annual growth rates over the next 20 years. That is massive growth, even before the region’s economies implement the reforms needed to make the aviation sector work better. Air travel simply must grow on Continent as its population pushes towards 3 billion over 30m square kilometers (more than three times the size of the United States).

Full implementation of commonsense policies (like SAATM) would reduce fares by 35%, and increase traffic by 51% to 141%. The IATA actually nails it when it comes to what African policymakers need to do to improve the aviation sector:

Recognize aviation as a strategic economic enabler—not a revenue source—and avoid excessive taxes and charges.

Invest in efficient, scalable infrastructure without passing unsustainable costs to airlines and travelers.

Facilitate market access and competition by advancing the implementation of the Yamoussoukro Decision and SAATM.

Improve affordability and strengthen connectivity to unlock wider economic and social benefits.

To these four I’d add one more recommendation: African economies should grow faster in order to firm up regional demand for air travel, cargo haulage, and related services. The confluence of high demand and resilient airlines (supported by the right policies) is the only way regional airlines — whether publicly-owned or private — can begin to catch up with the unforgivingly brutal economics of the airline business. Stated differently, good policies will achieve little if the region lacks large and reasonably profitable firms in the aviation sector.

II: On Africa’s many failed national flag carriers

As noted above, the problem of costly air travel in Africa isn’t just about politics and policy (although clearly both are a huge part of the problem). It’s also about the economics of Africa’s airlines as firms. At a fundamental level, it’s impossible to have decent connectivity across the Continent without well-run airlines. Therefore, it’s worth examining why many African airlines failed in the last 60 years.

At independence, lots of African countries established “national flag carriers” as prestige (as opposed to strategic) projects. These national carriers came at the expense of regional market consolidation, and the pooling of scarce capital as well as technical and managerial know-how.

Over the next 30 years most of these carriers failed. The varied trajectories of these airlines offer important lessons on the process of economic development, including technological transfer, upgrading of human capital and managerial competence, the importance of exposing national champions to external competition, how young firms (fail to) manage external shocks, and how successful national champions navigate their domestic political economies.

For the most part, African airlines were simply not prepared to survive the brutal economics of the aviation industry. Nearly all failed due to indisciplined management, chronic under-capitalization, unfavorable macroeconomic conditions, and, to be honest, bad luck with external shocks (read your Mkandawire, people!)

Having been founded largely as state-owned prestige projects (as opposed as strategic enterprises), African airlines were routinely saddled with politically-exposed individuals without much experience in the industry; and who run the airlines like any standard SOE that officials could raid for cash or use as conduits for looting public resources. An infamous example is Cameroon’s “Albatross” scandal, in which CamAir was used to purchase an aging Boeing plane (masked as new), and which President Paul Biya used exactly once. Cameroon lost $31m. Beyond such scams, most African airlines were required to create lots of superfluous jobs, a requirement that ate into already thin margins. For example, Nigeria Airways went belly up with over 750 employees per aircraft. Similarly, at its demise in 2002 Air Afrique had 4000 employees operating a single aircraft. The industry standard is 95-160 for highly-efficient carriers; budget airlines do as low as under 50 employees per aircraft. Airline operations were not spared either. State officials routinely commandeered aircraft for personal use; or booked seats for friends and family and simply didn’t pay. Officials running late would delay departures without care.

Then there was the brutal economics of the aviation business. Volatile energy markets (especially after the early 1970s) and the macroeconomic crises of the 1980s proved fatal for most airlines — fuel costs make up about 30% of airline’s operating expenses, requiring expert risk management and regular capitation (and some luck). The proliferation of flag carriers serving fragmented small markets foreclosed on the possibility of building resilience through scale. West African Airways Corporation, East African Airways and Air Afrique should’ve been given a fighting chance. The resulting defensive protectionism of inefficient airlines operating in small markets only amplified the costs of poor umanagement and state interference.

The biggest challenge of all to African airlines was chronic undercapitalization. The economics of airlines is such that firms routinely need capital injections to weather shocks such as fuel price hikes, geopolitical crises that halt travel, disease outbreaks (see Ebola and COVID), terror attacks that diminish demand, and the like. This on top of the fact that the business is capital intensive. Airliners cost a lot of money. So if you are a poorly-run airline, operating in a tiny market, in an economy characterized by severe macroeconomic risks (including forex risk) and poor demand, and whose sovereign has awful credit, you’ll naturally struggle to raise cash in the credit markets (or do so at unsustainably high rates). It doesn’t help matters that the little cash that you accumulate will typically be raided by public officials that treat you as a cash cow.

Chronic low capitalization directly impacts operations. If you can’t buy new planes you’ll have to operate old ones that consume more fuel and require more downtime for maintenance (both bad for your bottomline). This gets worse if you lack enough engineering capacity in-house, and have to outsource your maintenance operations. Couple this with any delays in getting parts through supply chain disruptions (you’ll likely not be your manufacturers’ priority), and you can see how having an old fleet can severely strain operations (and lose customers, thereby increasing costs). And because of your risk profile, any leasing agreements will typically come with higher costs. The net effect is that you’ll have to charge higher ticket prices, accept losses, or find yourself in the terrible position of doing both. The point here is that this isn’t an industry for poorly-run SOEs; even relatively better run private airlines in bigger, richer markets routinely go bankrupt because of the brutal economics of the sector.

III: Can air travel in Africa be fixed?

The simple answer is yes — if African policymakers can figure out how to (1) coordinate on opening up the region’s skies; and (2) incentivize the emergence of well-run airlines that are resilient to shocks.

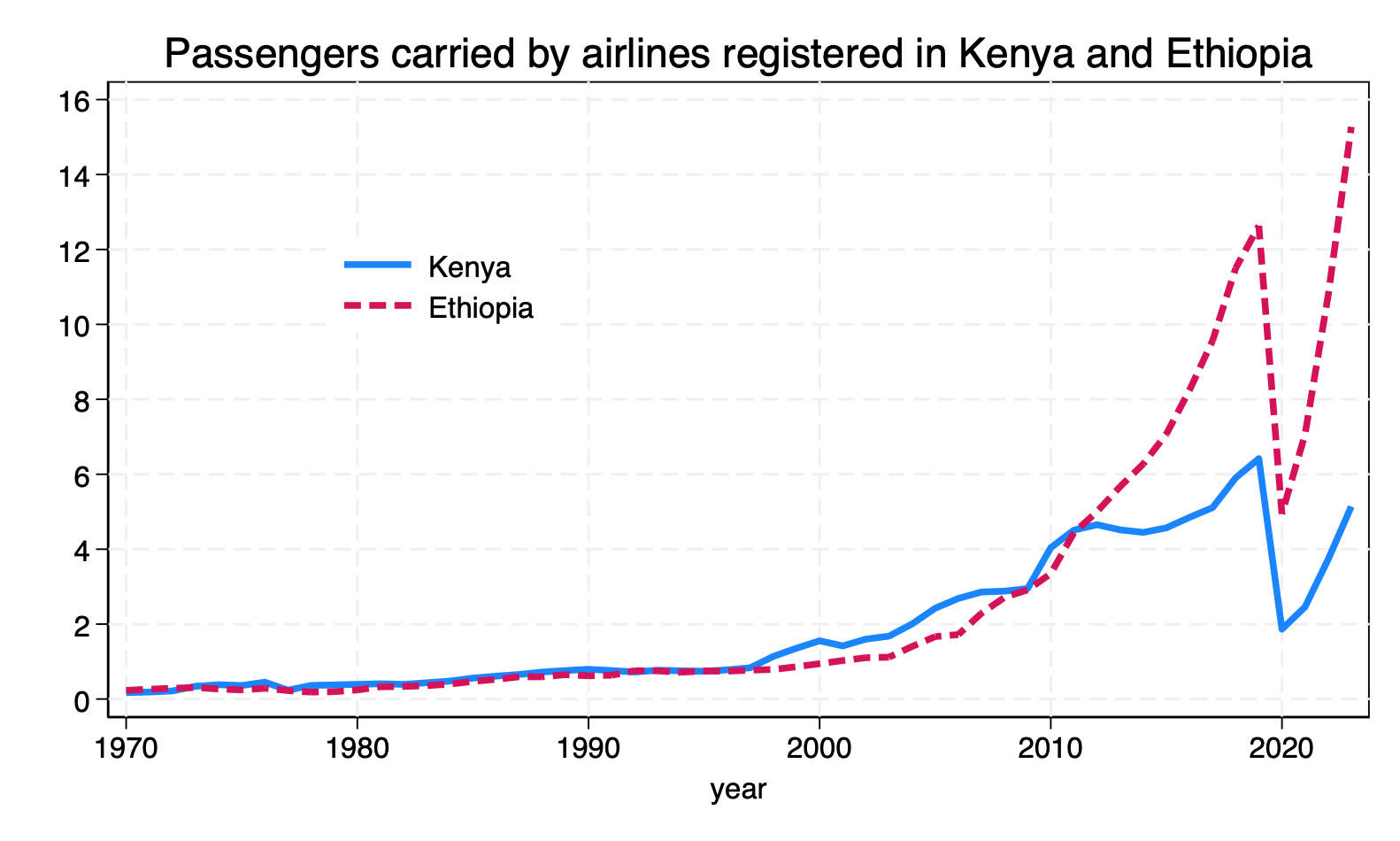

The all important resilience to shocks will have to be founded on large markets, diversified revenue streams, managerial excellence, and a deep capital base. Unfortunately, there is no set formula for getting these. For example, cross-country collaboration (which ostensibly secured large markets) did not spare Air Afrique and East African Airways from mismanagement before their collapse. Similarly, publicly-owned Ethiopian Airlines has done much better than Kenya Airways (which was privatized in the mid 1990s).

Everything will come down to whether airlines, qua firms, are robust to the brutal economics of the aviation industry, and resilient to shocks. It shouldn’t matter how they get there.

A tale of two airlines’ ambitious expansions

Here, it’s worth considering discussing concrete examples — the cases of Kenya Airways (KQ) and Ethiopian Airlines (ET).

KQ began operations in 1977 as an SOE following the collapse of East African Airways. After 15 years of losses, the airline emerged as one of the 45 prime SOEs for privatization in the early 1990s. In 1995 the government sold 26% of its shares to KLM (a Dutch airline), with a public listing of 51% of shares coming in 1996. The recovery after the 1990s restructuring, commercialization, and sale was such that 15 years later KQ embarked on a debt-financed $3.65b rapid expansion, with new routes and an almost doubling of aircraft under operations

That’s when the proverbial rain started beating KQ. Poor luck with the timing of external shocks and operational huddles (Ebola, terror attacks, fuel volatility and a hedging bet gone awry, a massive fire at its main hub, late delivery of Dreamliners) soon pushed the airline into the red. Suddenly, a growth strategy that was meant to catapult the airline to the next level looked like a careless bet that fundamentally misunderstood the industry. Accusations of corruption and mismanagement surfaced. CEOs came and went. Since 2011 KQ has gone through five failed restructuring strategies and had as many CEOs. Last year, it made a loss of $132.3m. Contributing to the loss was the grounding of three aircraft due to supply chain delays for parts and rising cost of fuel.

KQ’s failure to launch and perennial losses provide a sharp contrast to ET’s successes.

Ethiopian Airlines began operations in 1946 under an operational contract with America’s TWA (Trans World Airlines) — see the history here (Chapter 11) and here. Between 1946-1975 the airline went through a process of accumulating capabilities, from engineering know-how, operational competence, managerial excellence, and how to navigate the vagaries of the aviation sector. The decades under TWA enabled the airline to survive the Ethiopian civil war (1974-1991), especially the first five years of Derg rule (which came with significant managerial interference). In 1980 it got a new independent CEO and successfully resisted the Derg’s attempt to have it switch from Boeing to Soviet planes in the 1980s.

Following the war, ET focused on recovery, consolidation of its accumulate technical, managerial, and operational competence, and modest modernization. It also had to navigate a new political dispensation that came with its own set of management interferences. It took the appointment of seasoned insiders to determine the airline’s strategic organizational posture as an SOE that was nonetheless run commercially. This set the stage for its ambitious growth plans after 2000. ET’s growth focused on new equipment, a wider network of destinations, partnerships with other African airlines to unlock subregional connections, and diversification of revenue streams.

The diversification strategy would eventually yield the Ethiopian Airlines Group — a conglomerate that now includes the international airline, a domestic express service, airport ground services, a cargo and logistics business, catering and hospitality services, an aviation academy, and an MRO (Maintenance, Repair and Overhaul) division. While these ancillary businesses initially served ET, they’ve since evolved into independent revenue streams that serve other airlines — therefore becoming a source of resilience. For example, during COVID, ET’s MRO division quickly repurposed passenger planes into freighters, a move that enabled the airline to unlock new partnerships and revenue streams at reasonable cost.

What explains the divergent paths of ET and KQ?

ET’s advantage derived from its founding as a strategic national asset, the decades of accumulated technical, managerial, and operational knowledge under TWA, and ability to execute its strategy of resilience through diversification (as well as some luck). Geography then conspired to keep politicians honest and committed to the idea of ET as a national asset. In the 1940s the logic was that air travel would connect the country’s far-flung regions before road/rain infrastructure came online. More recently, land lockedness has amplified the need for a working airline as the country doubles down on high-value exports.

All this meant that the airline’s growth over the years has been gradual; and mostly driven by a firm grasp of industry fundamentals as opposed to consultant-driven wishful thinking. Furthermore, as a national strategic asset, ET was enabled by the Ethiopian government to grow and build sources of resilience — especially the vertical integration with ground operations. Unusually for an SOE, throughout its history periods of mismanagement and negative state interference have been the exception rather the rule.

The same cannot be said for KQ. In many ways, KQ has been a victim of poor timing. Its founding in 1977 came a time when the Kenyan state had lost its strategic coherence and policymaking capabilities (which peaked in the early 1970s). By then the aging Jomo Kenyatta had delegated the running of the state to his kitchen cabinet, most of whom were focused on succession fights and diverting state resources. Barely four years later the economic crises of the 1980s hit. Even though KQ inherited the bulk of East African’s equipment and operational know-how, the new airline could have used more time getting absorbed as a strategic SOE before the 1980s crisis (plus it didn’t help that East African wasn’t a particularly well-run airline to begin with). The timing of the 2011 expansion drive was also inauspicious (although it also reflected an absence of prudent management).

Once privatized, KQ was always going to struggle to build the same sources of resilience as ET did. This is for the simple reason that all those moves would’ve required scarce capital and managerial competency that a private company would view as wasteful and outside its core competency. It didn’t help that there was deep public distrust of the airline and its management after decades of losses and credible accusations that it was used as a conduit to loot public resources. For example, Kenyan legislators’ proposal to merge the airline business and airport operations into an “Aviation Holding Company” was met with little enthusiasm. The idea that KQ, in whatever form, would simply be used to loot state resources is a barrier to policymakers viewing the airline as a strategic national champion.

IV: Conclusion

One of the more exciting airline ventures on the Continent is ASKY, based out of Lome, Togo. The airline — which connects much of West and Central Africa — started life in 2010 under 40% ownership by ET (which has an operational contract to run it); as well as West African governments and private investors. ASKY has since grown to carry more than a million passengers, with 30 destinations in more than 27 African countries (served by 16 aircraft).

As argued above, ventures like ASKY are a reminder that there is no single formula for success in the airline business (e.g., state vs private ownership). What is important is that airlines are managed properly and made resilient against the brutal economics of the industry. Indeed, it is encouraging that the government of Togo has stepped up efforts to help ASKY bolster Lome’s stature as a regional hub. In this regard, ASKY may provide a model for future growth of the airline industry in Africa. If big countries insist on wasting money on poorly-run national flag carriers, relatively smaller countries can help create more efficient Pan-African airlines like ASKY. In Eastern African, RwandAir’s big bet with the new airport and collaboration with Qatar Airways is one to watch (I should also say that I am not so excited about the renewed efforts to build national carriers in the region. So far they all seem to be replicating the same SOE mistakes of the past).

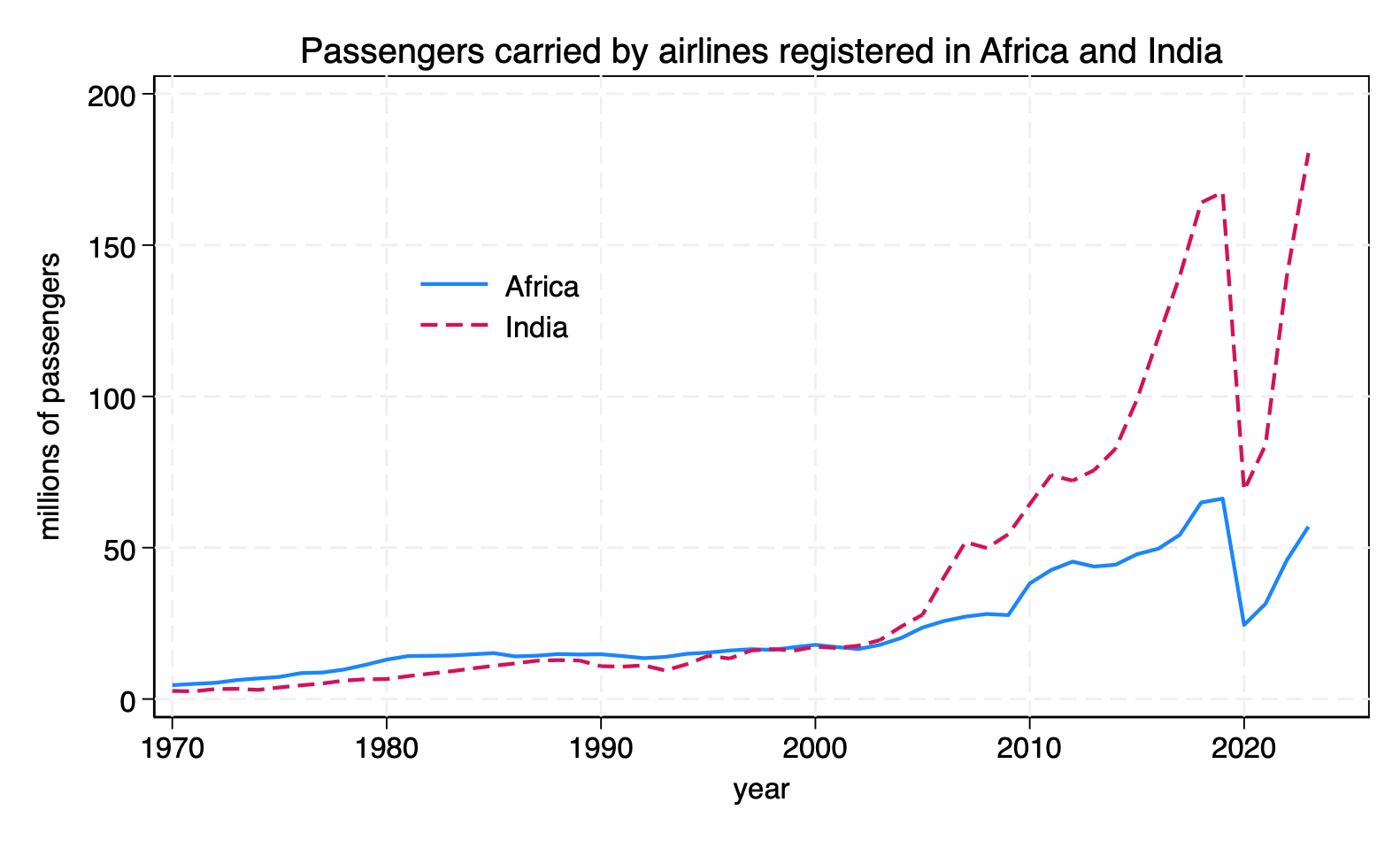

Growth will also help a great deal. For example, the divergence in passenger numbers between India and African countries (see figure) is, to a large extent, a growth story. As African economies expand and household incomes rise, Africans will fly more, thereby boosting demand and (hopefully) the region’s airlines’ margins. This has been the Indian story over the last two decades:

In India and much of South Asia, aviation demand moves in tandem with economic growth. Rising incomes, upward mobility, and the emergence of a new middle class directly translate into higher air travel affordability and usage. Air travel demand in the region is shaped by several factors, including per capita incomes, foreign direct investment, flight frequencies, and jet fuel prices, but income effects arguably remain the most decisive driver. With a young population and household incomes expected to approach USD 35,000 by 2030, India's demand base is structurally strong. In this light, large aircraft orders and aggressive capacity expansion plans are not speculative; they reflect an aviation market where demand fundamentals and economic realities clearly add up.

All this to say that while a lot of attention about the difficulty and cost of air travel in Africa focuses on policy failures (and they are many), it is also important not to lose sight of the fact that African airlines and how they are run as firms are also an important part of the problem. Therefore, getting costs down and rationalizing connectivity will require more than just policy. The region also needs better managed airlines that are resilient to the brutal economics of the aviation industry, and whose demand is anchored on thriving economies.

I once booked a short Uganda Airlines flight where the ticketing process made it seem like no pieces of luggage were included. I added it for an extortionary $100 (on a $400 flight) but then the ticket itself said this $100 was for a third bag (which I did not need). Getting this charge taken off proved impossible as I was bounced between individuals who took weeks to answer and were not empowered to do anything by their software. Such is life.

Ethiopian has been good to me for 10+ years, however. I expect them to become the Turkish Airlines of Africa in 20 years.

Aviation and African politics, two of my pet interests! Let me add some color to why Ethiopian is successful from a business point of view:

1) They very early on identified that Africa-China travel and trade was going to boom, and from the late 2000s started building up their network and sales distribution in China. ET flies to more Chinese cities than basically any other non-Asian airline. They dominate Africa-China corridors in both directions with both passengers and freight. They've since started building up in the Gulf as migration and trade links with the continent grow - basically, wherever Africans want to go, ET serves.

2) They leverage network effects to their maximum extent. Bole Airport is so busy precisely because ET schedules all of its flights to land and take off at the same time to maximize connections. Often that makes ET the only 1-stop option between many city pairs. They run Asky the same way - everyone arrives in Lome around the same time, everyone takes off between 1 and 2 hours later. No other African airline matches their operational discipline. Uganda Airlines, for example, has mostly random timings and odd 4 or 6 hour connection windows, so they are really only competitive with Ugandan passengers on direct flights, not connecting passengers.

Finally I think there are some factors to the rise of low-cost airlines in the West that are of interest to political scientists. Ryanair pioneered low-cost airlines that fly to secondary airports far from city centers - those airports were mainly disused military airfields from WWII that shifted to civilian control post-Cold War. Those airports offered lower taxes / fees (or acquiesced to Ryanair's demand for them) to attract more carriers - which drove down prices. Most African countries have never had to build infrastructure to fight air wars, and manage airports from a central national authority - which doesn't incentivize an enterprising local manager to build up low-cost services to an airport. Another case of wars make states...